- Crude oil rebound to over $17 fails to lift loonie.

- USD/CAD finishes week with small gain.

- Crude demand will remain weak until lockdowns lift.

Dollar Canada and the energy market

The dramatic recovery in oil prices after their even more dramatic collapse to below zero on Monday was not enough to revive the Canadian dollar which remains on the wrong side of the global risk trade and energy market.

Canada’s economy is more dependent on resource use and pricing than its southern neighbor and the oil market is in the midst of massive oversupply and crashing demand. North American shale drillers, a price war between Saudi Arabia and Russia and wholesale demand destruction from the pandemic business shutdowns have combined for the worst oil market in two decades.

The world is awash in oil. Storage capacity for crude is nearly full and refiners are even running out of places to put their unsold gasoline and jet fuel. Demand revival is contingent on the opening of the industrial world’s economies placed in deep freeze by the public health restrictions from the Coronavirus.

The spectacular but meaningless plunge in the West Texas Intermediate (WTI) May futures contract to -$40.32 on Monday is a fitting image for a global economy paralyzed by its response to the first modern pandemic.

The drama of Monday’s crude action should not disguise that the fact that the current WTI price is not unique. For almost a decade and a half, from early in 1986 until late 1999 WTI was below $20 about half the time and below $25 for almost the entire period.

Reuters

The advent of American and Canadian fracking production has tilted the pricing balance lower but the current supply glut is largely due to the shutdown induced collapse in demand. The reduction in use was not inevitable, it was the result of government action, nor is it permanent. Demand and price will revive as the global economic straightjacket is removed.

The USD/CAD opened the week at 1.4000 and finished on Monday at 1.4152 as WTI futures made their entry into the history books. Tuesday’s high for the week at 1.4265 came early in New York trading while WTI, which had recovered briefly to zero in late Monday trading, was again negative. By noon WTI was well above zero and the return to reality was well underway with high of $13.86 and a close at $10.01. The rest of the week in the energy markets was anti-climactic, WTI closed at $13.78 on Wednesday, $16.50 on Thursday and $16.94 on Friday. The USD/CAD drifted lower after Tuesday’s intra-day high closing at 1.4210, then 1.4161 on Wednesday, 1.4073 on Thursday and for the week at 1.4103.

Canadian statistics were limited to February retail sales which were better on the month at 0.3% than the 0.2% forecast though half the January rate. The ex-autos result was flat against a 0.3% prediction and a 0.1% gain in January. March inflation was weaker than estimated, likely a first indication of the decrease in demand from the job losses and social restrictions. Annual CPI was 1.6% against a 1.8% estimate and the core rate was 0.9% on a 1.2% forecast. Monthly rates were -0.6% and flat.

USD/CAD outlook

The Canadian dollar is under a double interdict.

Global markets prefer the US currency in any risk aversion scenario and the resource based Northern economy is facing a prolonged slump in commodity pricing and usage. Neither is amenable to the monetary policy remedies supplied by the Bank of Canada and at one remove by the US Federal Reserve. Their policies may ease the downturn and in the Fed’s case prevent financial system risk and contagion but they cannot create the demand necessary to lift the North American economies from their pending recessions.

Until at least one of the Canadian dollar’s disabilities, risk or energy demand, is removed its American cousin retains all the advantages.

Canadian statistics April 27-May 1

A thin week for Canadian data.

Thursday

The raw material price index for March. February was down 4.7% and January 2.3%. Gross domestic product for February is expected to be 0.1% as in January.

Friday

Markit manufacturing PMI for April, March was 46.1, February 51.8.

Canadian statistics conclusion

Canadian statistics for March in unemployment and PMIs have given a partial image of the impact of the pandemic on the economy. Like the US the full range of the disaster will not be seen until April but Canada does not have the advantage of the weekly jobless statistics that have, after the initial shock, prepared the US markets for the depth of the economic dislocation.

The April employment reports for both countries will be released on Friday May 8 and they will no doubt be gruesome but the accounting from Statistics Canada will likely provide a larger shock to the loonie.

American statistics April 20-24

Tuesday

Existing home sales, 90% of the US housing market, fell 8.5% to a 5.27 million annualized rate with many sellers pulling properties to await better conditions

Thursday

Initial jobless claims were 4.4 million in the week of April 10. This brings the total newly unemployed to just over 26 million in five weeks though claims are down 36% from their high of three weeks ago.

The preliminary IHS Markit purchasing managers’ indexes for April came in at 36.9 and 27 respectively, by far the lowest reading in the brief history of this series.

The Kansas City Fed Manufacturing Activity Index for April plunged to -62 from-18 in March. This is the worst level since the series began in 2001. In the 2008 financial crisis the lowest score was -32 that November.

Friday

Durable goods orders in March crashed 14.4% a bit worse than the -11.9% forecast but ex-transport orders were only down 0.2% on a -5.8% estimate and core capital goods orders rose 0.1% on a -6% predictions.

Michigan consumer sentiment for April was revised slightly higher to 71.8 from 71, a slip to 68 had been forecast.

FXStreet

US statistics April 27-May 1

Wednesday

First quarter GDP is expected to be negative at -4% driven down by the spectacular collapse in economic activity in March after running at about 2.7% in January and February as estimated by the Atlanta Fed.

Thursday

Initial jobless claims for the week of April 17 are forecast to be 3.5 million which would be a a 50% decline from the 6.867 peak on March 27.

Personal income in March should drop 1.4% following February’s 0.6% increase. Core PCE inflation will slip 0.2% to 1.6% and the headline index 0.1% to 1.7%.

Friday

The purchasing managers’ index for the manufacturing sector from the Institute for Supply Management is forecast to pitch to 36.7 in April from 49.1 in February. It would be the lowest score since March 2009.

US statistics conclusion

The labor market continued to dominate market perceptions. Having raised the bar for disaster to such extraordinary levels other data, like durable goods orders, existing home sales or the April non-farm payrolls, that might be expected to drive trading had or will have little impact.

In the week ahead initial and continuing claims remain center stage. The forecast 50% decline in claims will not be taken as good news given that it will bring the six week unemployment total to nearly 30 million. Likewise manufacturing PMI even if worse than predicted will have small import, though a better than expected number should be mildly positive for equities.

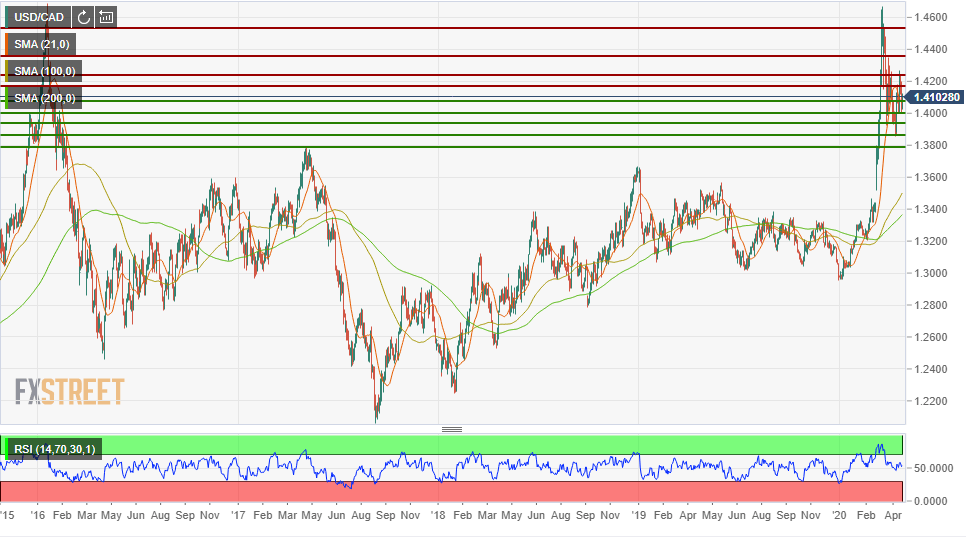

USD/CAD technical outlook

The relative calm of this week, WTI excepted, compared to the last month has given the relative strength index a mild positive indication but without conclusive trading signals. Likewise the three moving averages point higher with the cross of the 21-day on Monday with higher closes on Thursday and Friday pointing to USD/CAD gains next week.

Resistance: 1.4160; 1.4240; 1.4350; 1.4530

Support: 1.4070; 1.4000; 1.3930; 1.3860; 1.3780

Despite the weak bearish view in the immediate future, 42% vs 33% the general outlook for the USD/CAD is higher. Even the neutral opinion in the one month, 45% vs 30% and 25%, still posits a higher forecast at 1.4120. The one quarter view is strongly bullish 52% vs 30% and as the USD/CAD climbs the forecast will rise with it. The change from last week’s indecision is notable.

Source from https://www.fxstreet.com/analysis/usd-cad-forecast-wtis-spectacular-but-meaningless-collapse-202004262225